Advertising or repre? Do you know the differences and tax implications?

- ETL SLOVAKIA

- Latest News ETL EAST

- Advertising or representation?

Advertising or representation

In practice, there is often uncertainty regarding entertainment and advertising expenses. Correctly distinguishing between these expenses is key to their dtax treatment and accounting classification. In this brief overview, we provide a clear explanation to help you avoid mistakes and optimize your tax base.

Entertainment expenses – NOT a tax expense

According to Section 21(1)(h) of the Income Tax Act, entertainment expenses (e.g., refreshments, hospitality, gifts without advertising) are not tax deductible, i.e., they do not reduce the tax base.

Notice

Although it is not a tax expense, it is an accounting expense - it is accounted for as an expense, but is excluded from the tax base.

Typical examples:

business lunches and dinners with business partners,

gift baskets, chocolates, and other gifts without advertising labels,

non-alcoholic beverages (sweetened/sparkling water), coffee, and refreshments for visitors during meetings.

Expenses for employee drinking water may be tax deductible if they involve the provision of clean, still water (e.g., bottled water, barrel dispenser).

Advertising and promotional items – may be tax deductible

According to Section 19(2)(k) of the Income Tax Act, expenses for advertising and promotional items are tax deductible if:

- the value of the item shall not exceed 17 € excluding VAT per piece,

- it's not about alcohol or tobacco products.

We recommend that the item be marked with a trade name, logo, or trademark.

Príklady:

pens, calendars, notebooks, mugs, etc. with logo,

laptop/tablet cases with company logo printing,

wine (if the value does not exceed 5% of the tax base).

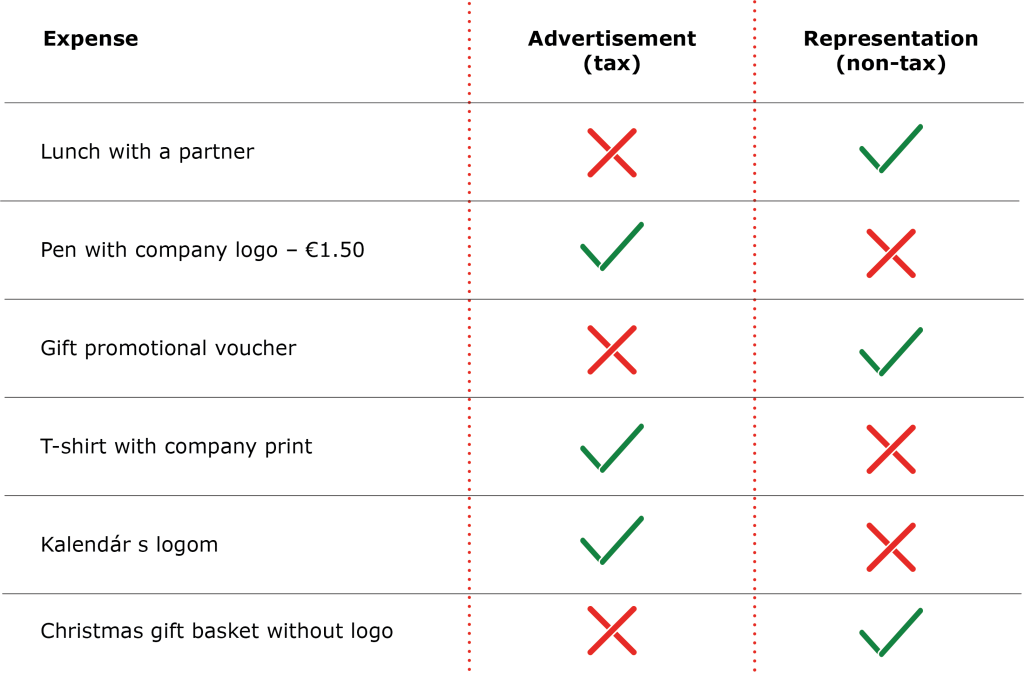

When is it advertising and when is it representation?

Video

In Slovak language.

Conclusion and recommendation

Distinguish well between representation and advertising.

Representation expenses are not tax deductible (e.g. hospitality, alcohol). On the other hand, promotional items (with a logo) costing up to €17 excluding VAT per item may be tax deductible if they are informational and promotional in nature.

Photo-document.

All expenses should be supported by photographic documentation or an advertising contract.

Watch the value limit.

If the item exceeds €17 per piece, it may be considered a gift rather than a promotional item, which changes its tax regime (e.g., VAT cannot be applied and the expense is not deductible).

Our Services

Expert services,

exceptional results

Our expertise is applied to every step of the process. We offer comprehensive services in tax, accounting, audit, and law, tailoring every aspect to fit your business needs.

Our goal is to provide you with stability, transparency, and success in an ever-evolving business environment.

Contact us

Looking for the optimal solution for your business needs? Contact us and we will take care of everything else with professionalism and care.